War in the Middle East and Market Resilience

- Note from the CIO

- Investment Management

The first quarter of 2026 was marked by an unusually high number of significant geopolitical events, including:

- January 3 – U.S. Army Delta Force captured Venezuelan President Nicolás Maduro and his wife; both are currently being held in Brooklyn.

- January 7 and 24 – Immigration and Customs Enforcement (ICE) fatally shot two U.S. citizens in Minneapolis.

- February 20 – The Supreme Court ruled that President Trump’s tariffs, imposed under the International Emergency Economic Powers Act, were unlawful.

- February 28 – The United States, in coordination with Israel, initiated major combat operations and widespread strikes against Iran, effectively closing the Strait of Hormuz and triggering a sharp increase in oil prices.

The extent to which such events influence global equity markets depends largely on two factors: how unexpected the events are and the degree to which they affect corporate profitability. Notably, international equities continued to outperform U.S. equities during the first quarter of 2026—a trend we previously identified as emerging last year.

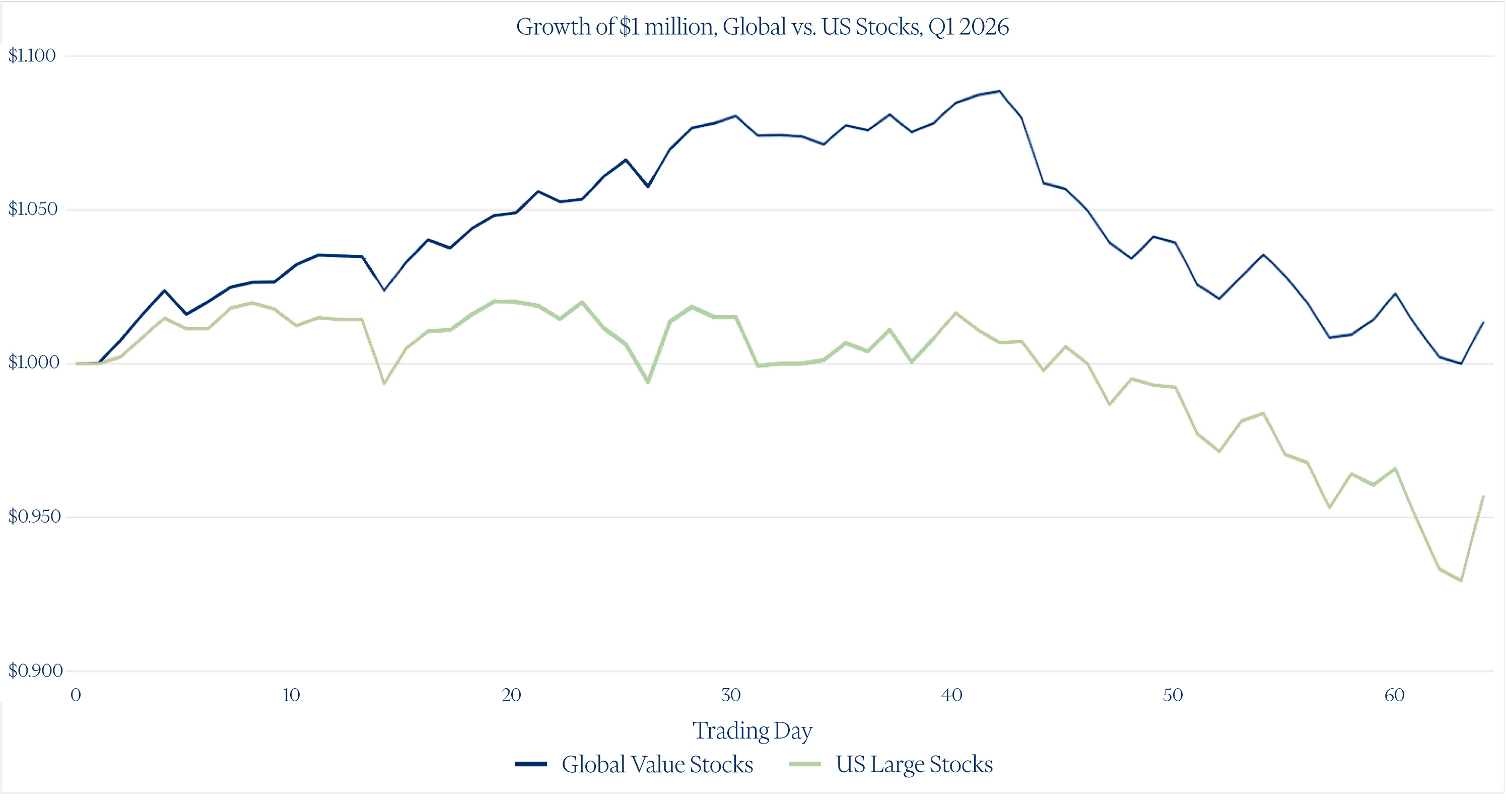

Across all major regions, relatively low-priced companies—commonly referred to as “value stocks”—outperformed broader market indices. The chart below illustrates the growth of $1 million invested at the beginning of the quarter in U.S. large-company equities versus a diversified portfolio of global value stocks (U.S. and international, across both large and small companies) over the 64 trading days of the quarter.1

Key Observations from the Data

Several points are worth highlighting:

- Despite the economic disruption caused by rising oil prices, global value stocks posted a gain of 1.3% for the quarter. While modest in isolation, this performance exceeded U.S. large-company stocks by 5.6%, as the latter declined by 4.3%.

- In recent years, U.S. and global market cycles have tended to peak and trough in close alignment. In contrast, during Q1 U.S. large-cap stocks peaked in late January (up 2.0%), while global stocks peaked in late February (up 8.9%)—coinciding with the onset of the Iran conflict.

- Although not shown in the chart, the top-performing equity asset class for the quarter was U.S. small-company value stocks. After lagging their international counterparts last year, they delivered a return of 5.0% in Q1.2

At first glance, it may seem counterintuitive that global equity markets produced even modestly positive returns during a quarter characterized by significant geopolitical shocks—particularly those affecting energy markets. However, context is critical.

Economic Context and Market Perspective

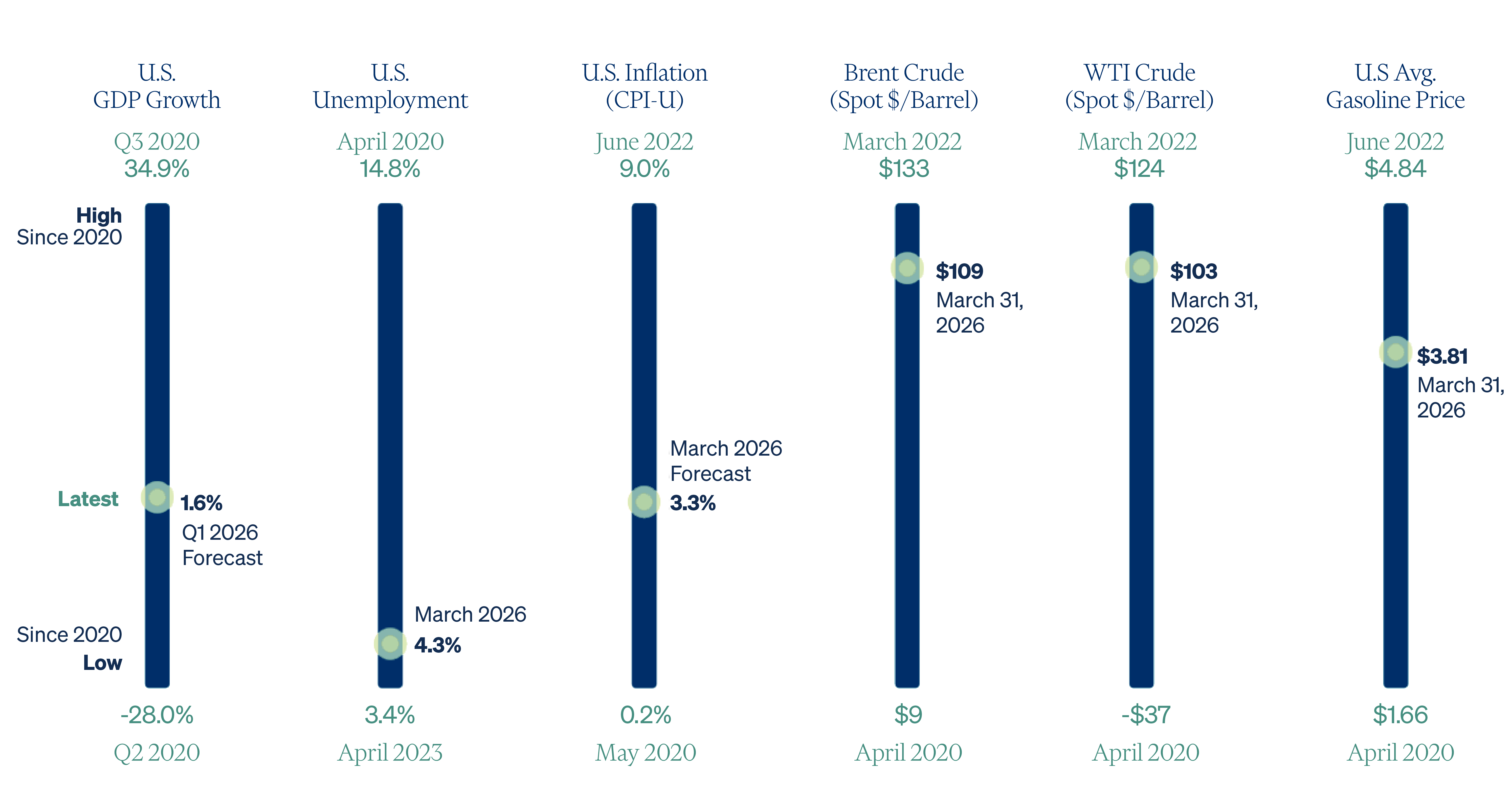

The following chart from Avantis Investors provides a broader view of key economic and market indicators from the beginning of 2020 (the onset of the COVID-19 pandemic) through the end of Q1 2026.

Economic and Market Indicators: High, Low, Current, January 2020 –March 2026

In this 7.25-year context:

- U.S. GDP growth is forecasted at 1.6%—not particularly strong but roughly mid-range relative to the period.

- The unemployment rate, at 4.3% as of March, remains near the low end of its historical range.

- The Federal Reserve’s benchmark interest rate, currently 3.5%, sits near the midpoint of its range.

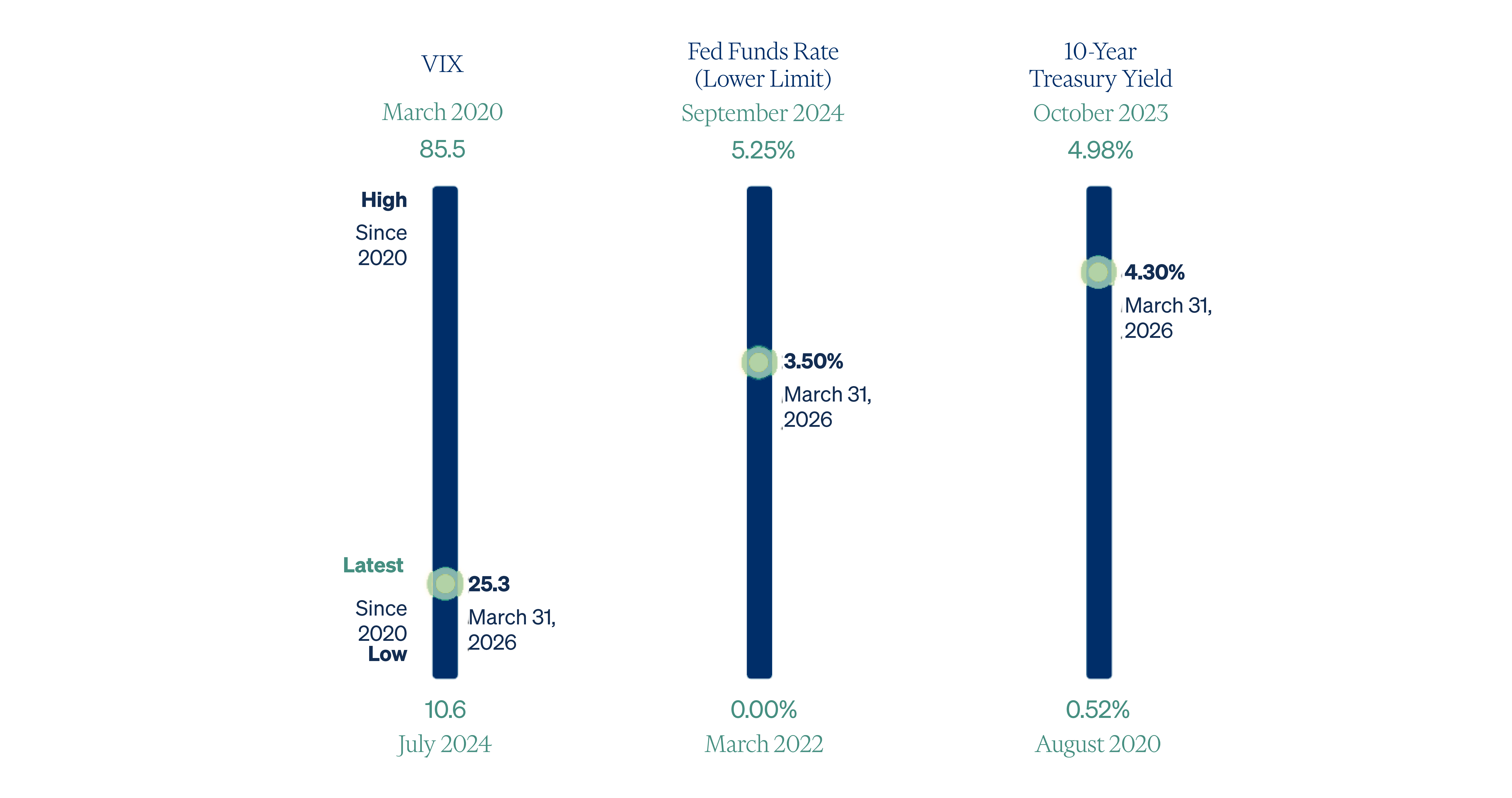

The CBOE Volatility Index (VIX), a widely followed barometer of expected near-term market volatility, peaked at 35.3 during the quarter (following the outbreak of the Iran conflict) and ended at 25.3. Neither level is especially notable when viewed in historical context.

A more concerning development is the level of longer-term interest rates. The 10-year Treasury yield currently stands at 4.3%, near the upper end of the range—potentially signaling expectations of persistently higher inflation and interest rates.

Among all indicators, energy prices warrant the closest attention. Both Brent and WTI crude oil prices are near the upper end of their range for the period, comparable to levels observed in early 2022 following Russia’s invasion of Ukraine. Rising energy costs tend to compress corporate margins and, in turn, weigh on equity prices—helping to explain the negative performance of U.S. stocks during the quarter. However, as a net exporter of oil, the U.S. also benefits from higher energy prices through increased profitability in the energy sector, which helped partially offset these broader market pressures.

Oil Prices and Market Expectations

Looking ahead, the trajectory of oil prices—and the broader implications of the Iranian conflict—remains uncertain. As of this writing, the U.S. and Iran have entered a two-week ceasefire.

According to the Federal Reserve Bank of St. Louis,3 WTI crude oil has averaged approximately $70 per barrel over the past 7.25 years. Current futures markets anticipate a price of roughly $74 per barrel by year-end.4 While market expectations often diverge from realized outcomes—particularly in the face of unforeseen events—they remain the most objective aggregation of available information at any given time.

Economist John Cochrane notes that both demand- and supply-side adjustments help mitigate the impact of rising oil prices.5 On the demand side, energy consumption can shift toward “substitutes” such as natural gas, nuclear, and renewables. On the supply side, higher prices (such as $100 per barrel) incentivize production from previously uneconomical sources.

Final Thoughts

In short, markets, companies, and economies demonstrate a remarkable capacity for adaptation in an ever-changing global environment. This adaptability is one of several reasons why investment decisions should not be driven by current events—particularly during periods of heightened uncertainty.

No one can reliably predict how geopolitical conflicts, energy markets, or global equities will evolve. For this reason, we continue to emphasize the importance of adhering to a disciplined investment plan, especially when uncertainty feels most acute.

- U.S. large companies are represented by the S&P 500 Index Total Return. Global companies are represented by the MSCI All Country World IMI Value Index (gross div.) Total Return. Data provided by YCharts ↩

- U.S. small-company value stocks are represented by the Russell 2000 Value Index Total Return. ↩

- Fred.St.LouisFed/series/DCOILWTICO ↩

- Oilprice.com/Futures/WTI/#CLV26, ↩

- TheGrumpyEconomist/WarandOil ↩

DISCLOSURE: Quantum Financial Advisors, LLC is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Quantum Financial Advisors, LLC by the SEC nor does it indicate that Quantum Financial Advisors, LLC has attained a particular level of skill or ability. This material prepared by Quantum Financial Advisors, LLC is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Advisory services are only offered to clients or prospective clients where Quantum Financial Advisors, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Quantum Financial Advisors, LLC unless a client service agreement is in place. This material is not intended to serve as personalized tax, legal, and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Quantum Financial Advisors, LLC is not an accounting or legal firm. Please consult with your tax and/or legal professional regarding your specific tax and/or legal situation when determining if any of the mentioned strategies are right for you.

Please Note: Quantum does not make any representations or warranties as to the accuracy, timeliness, suitability, and completeness, or relevance of any information prepared by an unaffiliated third party, whether linked to Quantum’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

For more information about Quantum and this article, please read these important disclosures.

- Note from the CIO

- Investment Management

Darius Gagne, PhD, CFP®, CFA

Darius Gagne is the Chief Investment Officer of Quantum Financial Advisors, LLC. Darius is also a Financial Advisor directly to clients and a founding partner of the firm.

Read More