Goal-Matching with Bond Ladders

- Note from the CIO

- Investment Management

As we enter the final quarter of 2025, I want to revisit the cornerstone of our goal-matching investment framework — bond ladders — which are an effective strategy for managing both equity market volatility and interest rate risk. Less widely appreciated, however, is that when used in conjunction with a goal-matching financial plan, they can also lead to greater long-term wealth compared to the traditional portfolio methodology that dominates current practice.

Equity Market Declines

Few events are more unsettling for investors relying on portfolio withdrawals than a sharp decline in equities — such as the 25% market drop caused by the inflation spike of 2022 or the 33% decline during the onset of the COVID pandemic. This is precisely where bond ladders provide stability by immunizing withdrawal needs.

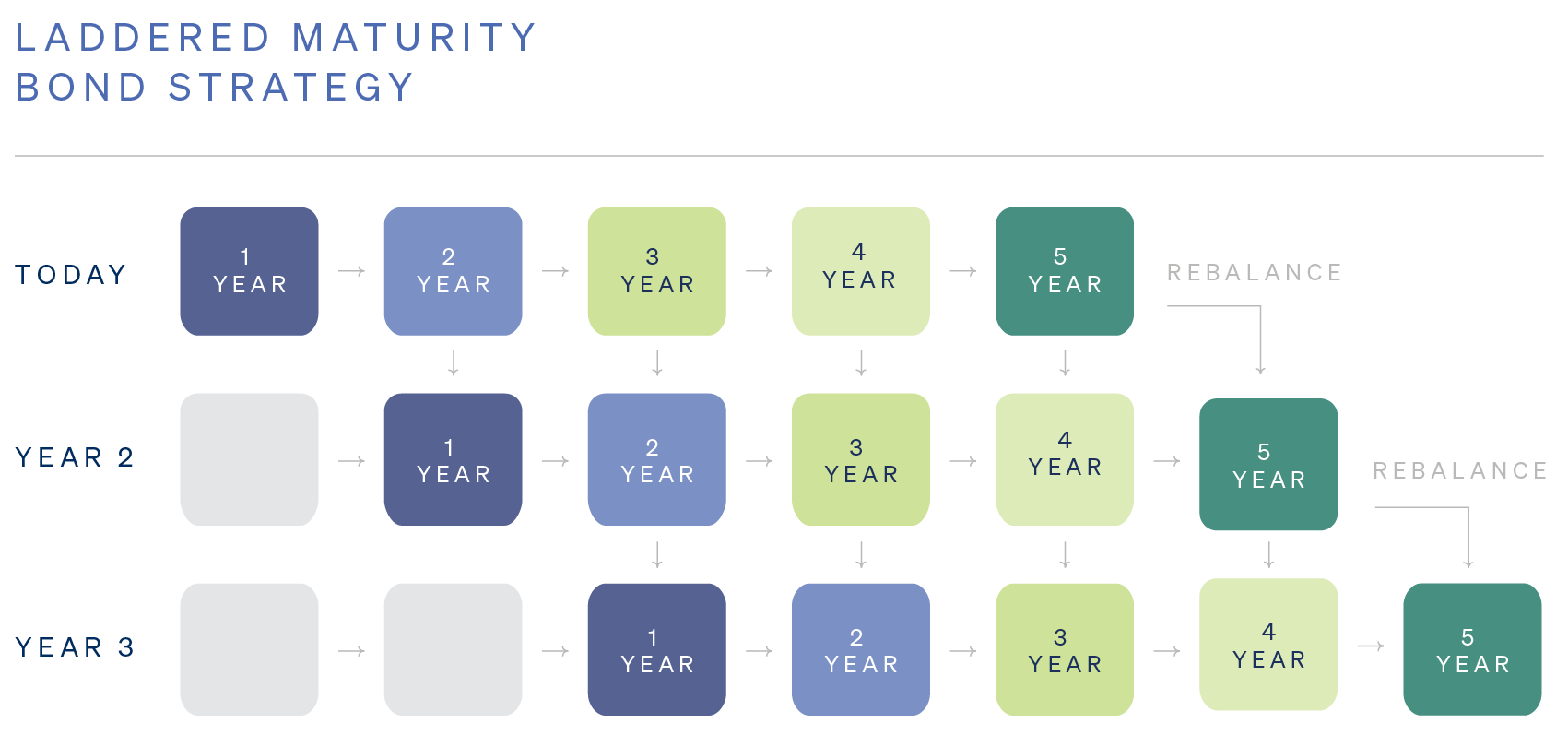

Consider a five-year ladder in which a $1 million bond allocation is divided into five $200,000 tranches maturing annually from 2026 through 2030. Historically, equities have advanced in roughly three out of every four calendar years — the S&P 500 has risen in 74 of the last 99.1 In most years, withdrawals can therefore be funded by trimming appreciated equities and, as needed, bonds maturing that year — maintaining the overall equity-bond allocation. At year-end, we extend the ladder by reinvesting the proceeds from matured bonds, along with a portion of equity gains, into a new fifth-year maturity (for instance, 2031 in this example). See an example illustration of a laddered maturity bond strategy below.

In years when equities experience significant declines, our goal is to avoid selling stocks at depressed levels. History shows equity downturns are temporary and markets are resilient. Withdrawals in such years are instead funded by the bonds maturing that year, allowing the investor to remain fully invested in equities until recovery even when emotions run high. This mechanism not only provides liquidity during downturns but also maintains disciplined rebalancing: as equities fall, the portfolio naturally becomes more bond-heavy, which withdrawals from the ladder gradually correct over time.

If equity weakness persists for multiple years, subsequent maturities can continue to fund withdrawals. A five-year ladder, for example, would have covered the drawdown and recovery periods during the 2008 financial crisis.2 Once equities recover, bonds can be replenished by selling appreciated equities to rebuild a full five-year structure.

Interest Rate Risk

A second major concern for retirees is rising interest rates, which reduce the market value of existing bonds. For example, a loss of confidence in the U.S. dollar could push yields higher. Yet this too is where bond ladders provide protection.

Because bonds within a ladder are held to maturity, their temporary price fluctuations are largely irrelevant to the investor’s cash-flow plan. As each bond approaches maturity, its price naturally converges toward par value — what is often called the pull-to-par effect. Thus, regardless of interim rate movements, the bond’s full principal value is available in the year it is needed for withdrawals.

Together, these two features — liquidity during equity downturns and maturity value stability amid rate increases — make bond ladders a powerful tool for risk management. But there is more.

Wealth Enhancement Through Goal-Matching

Now let’s consider how bond ladders integrate with our goal-matching framework to enhance long-term wealth.

Assume a total annual spending goal of $360,000 (indexed to inflation), divided equally among essential, important, and discretionary categories. Essential expenses — e.g., property taxes, insurance, and healthcare — can be hedged during a 35-year retirement with a $3.4 million bond ladder providing $120,000 per year. Important spending is funded through equities, supported by a two-year reserve of laddered bonds (about $240,000) to navigate an average-length bear market. Discretionary goals are invested entirely in equities. For a $10 million portfolio, this framework begins with an allocation of roughly 65% equities and 35% bonds.

By contrast, a traditional 65/35 balanced portfolio maintains fixed weights regardless of market direction, rebalancing systematically. When equities rise, rebalancing shifts capital into bonds, effectively holding expected portfolio returns constant year after year. This approach implicitly assumes that all spending — essential and discretionary — carries the same level of uncertainty, which is unrealistic. It treats essential needs too liberally and discretionary goals too conservatively, leading to a misalignment between priorities and risk.

A goal-matching design aligns asset allocation with the true nature of each objective: essential spending with bonds, discretionary spending with equities. Each passing year reduces the number of remaining essential-spending years, and therefore one rung of the ladder is removed annually. The equity share of the portfolio gradually increases as time progresses — a counterintuitive but logically consistent outcome. This is the opposite of conventional “glide path” wisdom, where bond exposure rises with age.

Our modeling suggests that, for the example above, this approach could result in approximately $7 million more in terminal portfolio value at the end of a 35-year retirement — equivalent to roughly the purchasing power of $3 million today.

There are many ways our advisors add value over time, but few contribute more meaningfully to a client’s financial security and legacy than thoughtful goal-matching implemented through disciplined bond laddering.

- The Bumpy Road to the Market’s Long-Term Average, S&P 500 Index Annual Returns 1926-2024, Dimensional Fund Advisors ↩

- Daily S&P 500 Index data provided by Yahoo Finance. We used the 4.5 year period from Oct 2007 - April 2011. The S&P 500 high was in Oct 2007. The index reached that value again with dividends included in April 2011. ↩

DISCLOSURE: Quantum Financial Advisors, LLC is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Quantum Financial Advisors, LLC by the SEC nor does it indicate that Quantum Financial Advisors, LLC has attained a particular level of skill or ability. This material prepared by Quantum Financial Advisors, LLC is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Advisory services are only offered to clients or prospective clients where Quantum Financial Advisors, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Quantum Financial Advisors, LLC unless a client service agreement is in place. This material is not intended to serve as personalized tax, legal, and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Quantum Financial Advisors, LLC is not an accounting or legal firm. Please consult with your tax and/or legal professional regarding your specific tax and/or legal situation when determining if any of the mentioned strategies are right for you.

Please Note: Quantum does not make any representations or warranties as to the accuracy, timeliness, suitability, and completeness, or relevance of any information prepared by an unaffiliated third party, whether linked to Quantum’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

For more information about Quantum and this article, please read these important disclosures.

- Note from the CIO

- Investment Management

Darius Gagne, PhD, CFP®, CFA

Darius Gagne is the Chief Investment Officer of Quantum Financial Advisors, LLC. Darius is also a Financial Advisor directly to clients and a founding partner of the firm.

Read More