The Double-Edged Sword of Concentrated Equity

- Executive Compensation

- Investment Management

Having spent significant time in Silicon Valley, I’ve had a front-row seat to some of the greatest cycles of innovation, wealth creation, and unfortunately, wealth destruction in modern history.

I have immense respect for the founders, executives, and early employees who worked incredibly hard to create real value for their companies and customers. Some of these individuals held onto their equity (and assumed significant risk), and some even benefited immensely by doing so, going against traditional financial advice to diversify.

A decade of massive valuations can easily create an illusion of invincibility. But confusing a booming tech sector with a guaranteed safety net is exactly how life-changing wealth gets wiped out overnight.

While concentration can build wealth, diversification is what preserves it. Because when the music stops, the damage can be catastrophic.

When "Sure Things" Implode

We have all seen companies that were widely considered “can't-miss disruptors” suffer massive implosions, wiping out the net worth of employees whose wealth and salary were tied to the exact same sinking ship. Here are a few recent examples:

- The Peloton Plunge During the pandemic, Peloton was the ultimate tech-fitness darling. Its stock rocketed to a record close of over $167 a share in January 20211 . However, as demand normalized, the stock cratered. By early 2026, shares were trading near $5, a devastating drop of over 97% from its peak2 .

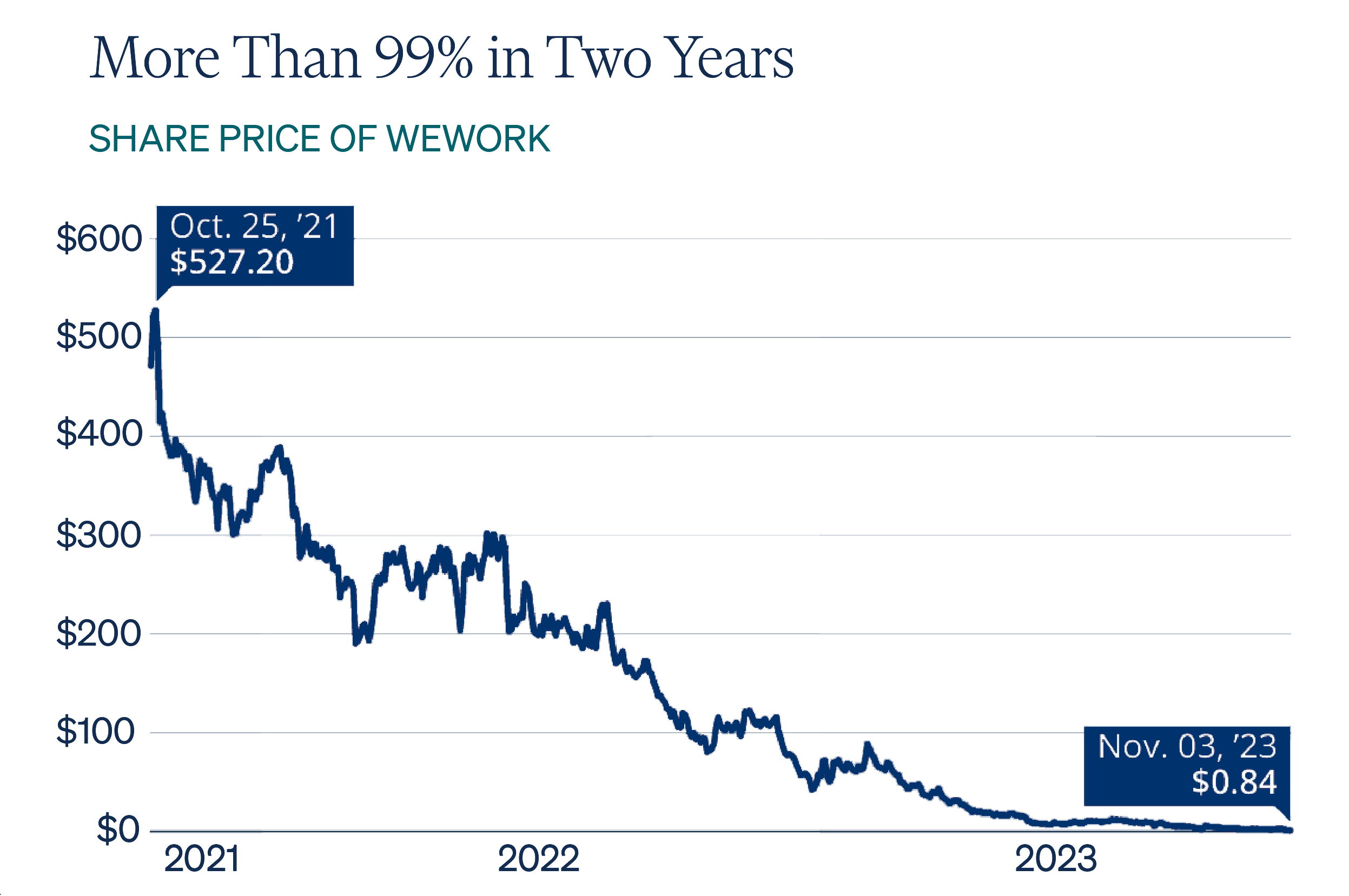

- The WeWork Wipeout In 2019, SoftBank privately valued the co-working giant at a staggering $47 billion 3 , making it one of the most valuable startups on the planet. Just four years later, in late 2023, after failed IPO attempts and massive cash burns, WeWork filed for Chapter 11 bankruptcy protection 4 , wiping out billions in employee and investor equity.

There are countless other examples.

The Executive Dilemma

Why do brilliant, analytical executives let this happen? In my experience, it almost always comes down to a lack of bandwidth.

Executives are so busy managing risks specific to their companies, building products, scaling solutions, and putting out fires, that they neglect their own personal risk management. They spend 60+ hours a week protecting their company's balance sheet, but who is protecting theirs?

The Quantum Approach: Asking the Big Questions

Dealing with concentrated stock isn’t a one-size-fits-all spreadsheet exercise. Yes, rational financial theory says you should "sell and diversify," but we live in the real world. The real world involves emotional attachments, tax implications, behavioral biases, lock-up periods, and company loyalty.

At Quantum, we take a methodical approach to selling concentrated stock shares to help our clients achieve a realistic balance. Sometimes, simply being able to answer questions like the ones below can be a revelation:

- If my company went to $0 tomorrow, would my family be okay?

- If I never earned another dollar going forward, what lifestyle could my current portfolio support?

Because no single client situation is the same, we create financial plans for our clients and we stress-test them for a myriad of market environments and variables. Before we make a single trade, we can illustrate what would happen to lifestyle needs, wants, and wishes if a concentrated position took a 20%, 50%, or larger hit. Could essential needs still be reliably covered? What would happen to the "nice-to-haves" and discretionary goals?

Our planning process helps map financial resources directly to individual priorities by separating assets into two distinct buckets: Critical Capital (the non-negotiable funds needed to maintain lifestyle and survive) and Surplus Capital (such as the moonshot goals fund or leaving a legacy fund).

For a deep dive into how we secure that first bucket so essential cash flows can be immunized regardless of what a concentrated company stock (or broader stock market) does, I highly recommend reading Darius Gagne’s breakdown, “Goal Matching with Bond Ladders.”

However, to build the diversified portfolio that ultimately secures the required Critical Capital, we often need to take some chips off the table. Transitioning wealth out of a concentrated position is where specialized strategies can come into play.

The Deconcentration Toolkit

Today, there are a myriad of tools available to manage concentration risk without necessarily triggering massive, immediate tax bills. To build the foundation that protects Critical Capital, a customized strategy might include options such as:

- Strategic Outright Sales: Sometimes the best solution is the simplest. We help create a capital gains budget and put a disciplined exit plan in place to gradually sell shares and reduce single stock exposure over time.

- 10b5-1 Plans for Officers, Directors, or Major Stockholders: Setting up an automated, compliant selling schedules to remove the emotion and legal risk from trading.

- Securities-Backed Lines of Credit (PALs): Accessing liquidity to build a diversified portfolio without selling shares immediately.

- Exchange Funds: Restricted to accredited investors, an exchange fund can serve as a powerful diversification tool by pooling concentrated public stock positions into a single diversified fund, which must maintain at least a 20% allocation in private real estate. Investors face high entry barriers—typically $500,000 to $1 million minimums—and will receive a Form K-1 for tax purposes.

- Options Strategies (such as Collars): Setting up a hedge (insurance) against downside risk. (Trading options involve significant financial risks, including the possibility of losing the entire initial investment if market conditions are unfavorable. Some advanced strategies, especially those involving uncovered positions, can expose a trader to substantial losses.)

- Philanthropic & Legacy Transfers: Gifting appreciated positions to a donor-advised fund, a charity, or other beneficiaries to reduce taxable estate.

- Long-Short Tax-Aware Funds: Utilizing specialized investment funds to hedge sector- or company-specific risk while actively harvesting tax losses that can be used to offset the capital gains concentrated shares are eventually sold.

The nitty-gritty mechanics of every tool in the toolkit are beyond the scope of this blog post. The most important question we answer before implementing any strategy is simply this: Does this strategy actually make sense for your financial plan? We need to ensure it moves the needle in the right direction while aligning with your risk tolerance, tax situation, and overall costs.

If your net worth is tied up in the company ticker you look at every morning, contact your Quantum advisor, who can help you build a safety net. Your Quantum advisor will evaluate your situation and guide you to make the best decision for your unique situation.

DISCLOSURE: Quantum Financial Advisors, LLC is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Quantum Financial Advisors, LLC by the SEC nor does it indicate that Quantum Financial Advisors, LLC has attained a particular level of skill or ability. This material prepared by Quantum Financial Advisors, LLC is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Advisory services are only offered to clients or prospective clients where Quantum Financial Advisors, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Quantum Financial Advisors, LLC unless a client service agreement is in place. This material is not intended to serve as personalized tax, legal, and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Quantum Financial Advisors, LLC is not an accounting or legal firm. Please consult with your tax and/or legal professional regarding your specific tax and/or legal situation when determining if any of the mentioned strategies are right for you.

Please Note: Quantum does not make any representations or warranties as to the accuracy, timeliness, suitability, and completeness, or relevance of any information prepared by an unaffiliated third party, whether linked to Quantum’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

For more information about Quantum and this article, please read these important disclosures.

- Executive Compensation

- Investment Management

Adam Salas, CFA, CFP®

Adam Salas is a Financial Advisor and Investment Committee member with Quantum Financial Advisors, LLC.

Read More