Navigating The Widow’s Penalty

- Financial Planning

- Tax Planning

- Estate Planning

For many high-net-worth couples, financial planning often centers on the accumulation phase—growing the nest egg and reaching retirement. However, as the focus shifts to the distribution phase, a structural flaw in the U.S. tax code begins to loom over surviving spouses: the Widow’s Penalty.

This penalty isn't a single line item on a tax return but rather a series of financial disadvantages that occur when a household transitions from "Married Filing Jointly" to "Single" filer status. Given that the probability of simultaneous death for a couple is near zero, this transition is almost a mathematical inevitability that, if unaddressed, can lead to a 10% or greater spike in effective tax rates.

The Mechanics of the Penalty

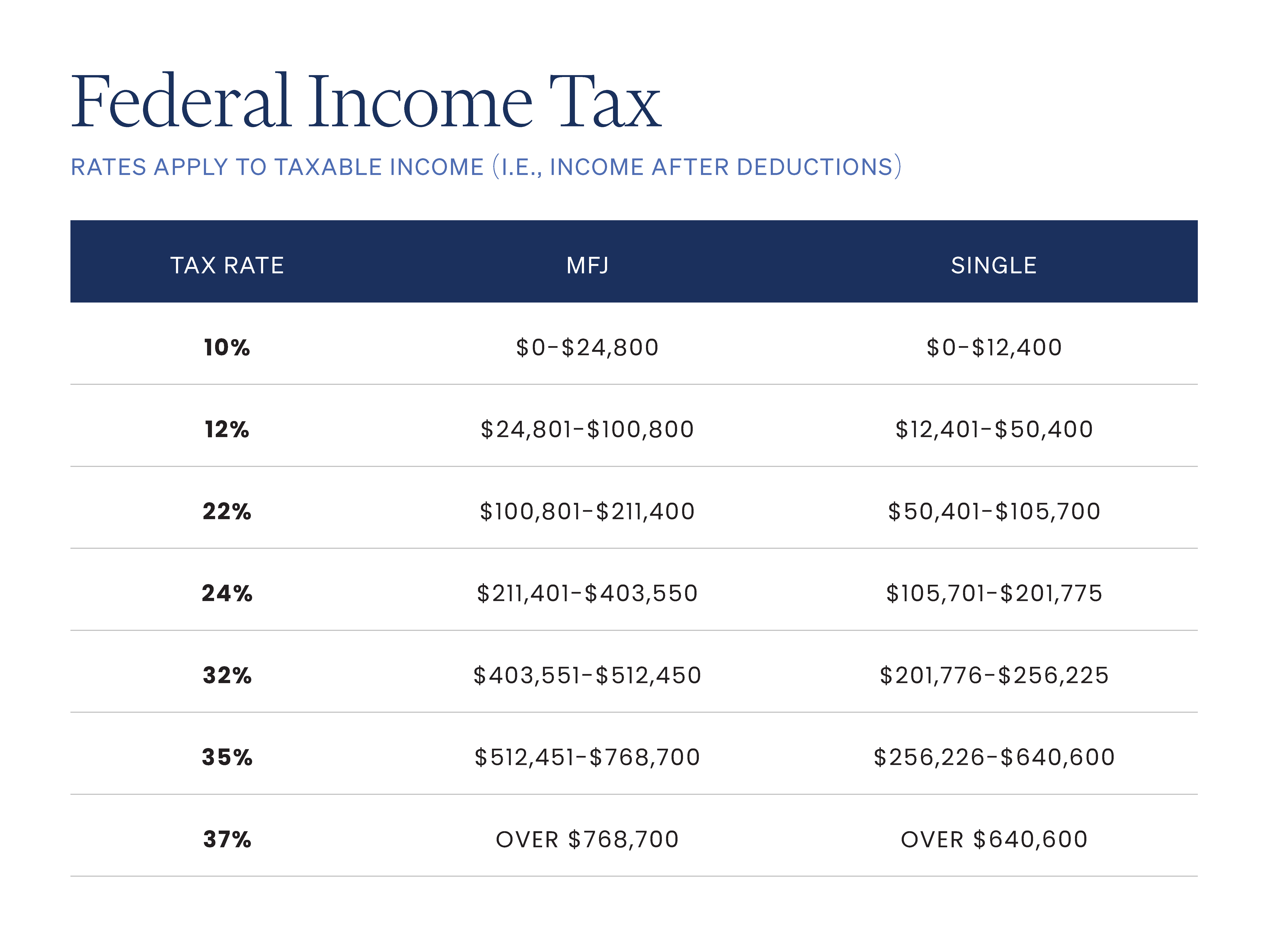

The primary driver of the Widow’s Penalty is the compression of tax brackets. While the surviving spouse can continue to file their taxes as Married Filing Jointly (MFJ) for the year of death, the change in tax status for the following year can have significant tax implications. The survivor’s standard deduction is cut in half, and simultaneously, the income thresholds for higher tax brackets shrink. For example, a taxable income of around $60,000 that is safely nestled in the 12% bracket for a couple might suddenly be in the 22% bracket for a single individual following the death of one spouse. (see table below)

Required Minimum Distributions (RMDs)

The penalty is exacerbated for those with large traditional IRAs. RMDs are calculated based on the account balance at the end of the year and the age of the account owner, not their filing status. As a result, the surviving spouse inheriting a large IRA must continue taking substantial distributions, which are now subject to tax at the much higher single-filer rates.

Income Related Monthly Adjustment Amount (IRMAA) Surcharges

The income thresholds for Medicare Part B premiums and Part D surcharges for single filers are half that of married filers. As a result of this significantly lower threshold, the surviving spouse may find themselves facing the single-filer "cliff" and paying hundreds of dollars more per month for health insurance. For example a married filer with $200,000 in modified adjusted gross income (MAGI) would pay $202.90 per month for Part B and $0 for Part D. A single filer with that same $200,000 in MAGI would see their part B and D premiums jump to $527.50 and $60.40 respectively. 1

Loss of Senior Deductions

Similar to the single filer cliff mentioned above, the enhanced standard deductions for seniors are phased out more quickly at lower income levels for single filers.

Planning Opportunities

Now that we have covered some of the common pitfalls, let’s explore a few planning opportunities you can take advantage of before you find yourself in the Widow’s Penalty box.

Strategic Roth Conversions

Roth conversions can be a powerful tool for mitigating the Widow’s Penalty. By executing large Roth conversions while both spouses are alive, couples can pay taxes at the lower joint rates reducing your IRA balance. This strategy effectively "shrinks" the future RMDs that would otherwise be taxed at the survivor's higher single rate as we touched on earlier.

Qualified Charitable Distributions (QCDs)

QCDs also offer a powerful release valve. For surviving spouses who are charitably inclined, making charitable distributions directly from the IRA to a qualified 501(c)(3) charity can satisfy RMD requirements without increasing your adjusted gross income (AGI), thus protecting the survivor from inadvertently moving into a higher tax bracket and incurring the higher Medicare IRMAA surcharges as mentioned above.

By strategically planning for your future and addressing the Widow’s Penalty head-on, families can transform a traditional IRA from a looming liability into a high-growth, tax-free legacy for their heirs. As always, your Quantum advisor is here to help you plan for situations like this so you can feel confident around your financial picture.

DISCLOSURE: Quantum Financial Advisors, LLC is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Quantum Financial Advisors, LLC by the SEC nor does it indicate that Quantum Financial Advisors, LLC has attained a particular level of skill or ability. This material prepared by Quantum Financial Advisors, LLC is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Advisory services are only offered to clients or prospective clients where Quantum Financial Advisors, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Quantum Financial Advisors, LLC unless a client service agreement is in place. This material is not intended to serve as personalized tax, legal, and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Quantum Financial Advisors, LLC is not an accounting or legal firm. Please consult with your tax and/or legal professional regarding your specific tax and/or legal situation when determining if any of the mentioned strategies are right for you.

Please Note: Quantum does not make any representations or warranties as to the accuracy, timeliness, suitability, and completeness, or relevance of any information prepared by an unaffiliated third party, whether linked to Quantum’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

For more information about Quantum and this article, please read these important disclosures.

- Financial Planning

- Tax Planning

- Estate Planning

Matt Higgins, CFP®

Matt Higgins is a Financial Advisor with Quantum Financial Advisors, LLC.

Read More